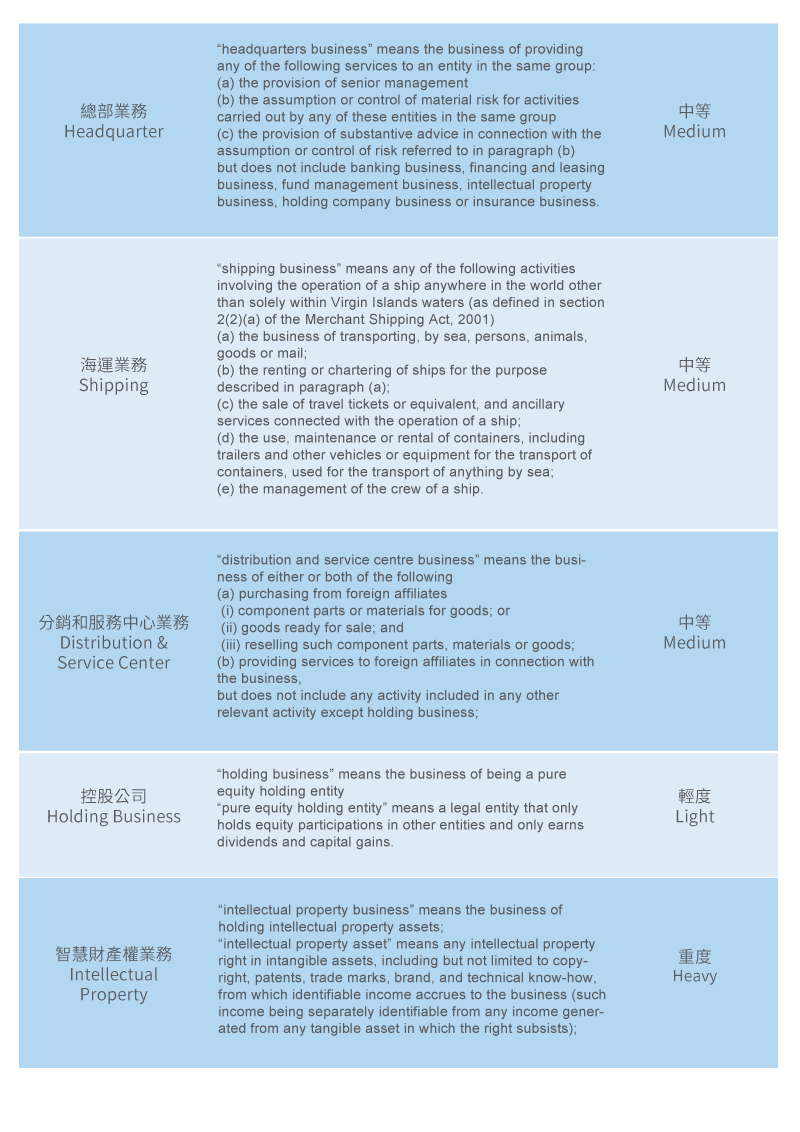

| 資料更新時間:2021/08/03 依規定BVI公司需每年於財政年度後六個月內完成經濟實體申報,需將BVI公司近期營運活動狀態更新申報,維詮並取得BVI ITA(INTERNATIONAL TAX AUTHORITY)經濟實體條例二版原文,以下資料配合更新並同步修正對於九大類經濟活動中〝控股公司〞、〝營運分銷(三角貿易)〞之認定標準。(*網頁版刪除部分內容) 若以經濟實體條例二版原文定義來看: 1、Holding business: “holding business” means the business of being a pure equity holding entity “pure equity holding entity” means a legal entity that only holds equity participations in other entities and only earns dividends and capital gains. 5.25 The definition of pure equity holding entity is deliberately framed in narrow terms. A legal entity will only fall within the definition if it holds nothing but equity participations, yielding dividends or capital gains. The ownership of any other form of investment (such as an interest bearing bond) will take the legal entity outside this definition. 5.27 Entities which own other forms of asset (eg bonds, government securities, legal or beneficial interests in real property) will clearly not be pure equity holding entities (even if they also own equity participations) and will not be treated as carrying on holding business. 無論是否取得子公司所分配之股利股息,只要符合單純控股即屬控股公司。 2、Distribution and Service centre business(配送與分銷業務、如以BVI公司操作三角貿易、移轉定價均屬此分類): “distribution and service centre business” means the business ofeither or both(*買/賣之一方或雙方)of the following

but does not include any activity included in any other relevant activity except holding business; 5.35 For an entity to carry on distribution and service centre business it must have a business which consists of purchasing assets from other entities inthe same group(*參酌會計上的定義,除同一人控制外也包含控制權), and/or a business providing services to entities in the same group. The affiliates in question must be “foreign” – that is to say an affiliate which is an entity which is not a legal entity for the purposes of the legislation. 5.36 It should be noted that the following do not constitute distribution and service centre business: (a) the business of purchasing and reselling assets from, or providing services to, entities in the same group both of which are located in the BVI (b) the business of purchasing and reselling assets from, or providing services to, entities which are not part of the same group as the entity carrying on the business, even if located outside the BVI, or (c) occasional transactions within the description which do not form part of a business but are undertaken ancillary to a different business and such other activity is recharged at cost or less i.e. the legal entity does not profit from the other activity. (If the entity’s business falls within the description of a relevant activity, substance requirements would apply in respect of that relevant activity.) 依此定義,「移轉定價」的BVI公司屬九大類〝配送與分銷業務Distribution and service centre business〞活動,依規定必須在當地建構符合要求之CIGA(核心創收活動)。不是請一個人、租一間辦公室就沒事。

3、目前BVI ITA已針對申報為九大類經營活動、且需在當地具備CIGA、並未提供相關資料之BVI公司做調查。 4、維詮一再強調任何BVI公司經濟實體法之申報、後續之修正、違規與罰款、上訴等,都必須透過您的秘書公司、註冊代理人來協助方能進行。依據維詮的經驗,一旦違規後再想辦理移轉(由新專業團隊接手處理)將會非常棘手;原本的違規缺失與罰金必須由原註冊代理人完成繳納方能移轉。一旦違規才想移轉將會花費更多金錢與時間。

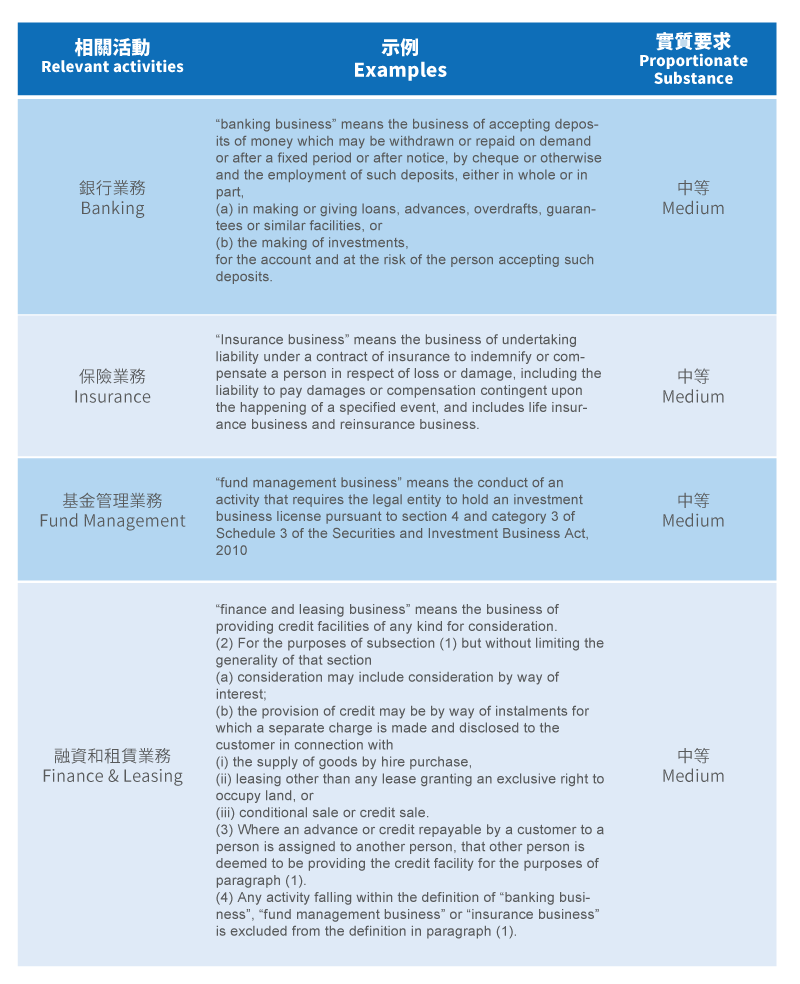

6、如果無法明確BVI公司所從事之活動是否符合經濟實體法9大類經濟活動,可以付費進行分類服務。 7、維詮所經辦BVI公司註冊代理人計有:Vistra、Newhaven、Harneys三家、均為國際專業註冊代理機構。 8、BVI經濟實體法所規管之九大類經營活動。以下定義以經濟實體條例二版內容更新。

9、境外公司服務鍊。

#OBU #BVI境外公司經濟實質申報 #經濟實質申報罰則 #九大類經濟活動如何處理 #轉BVI公司 |

- 財政部公告:預告「個人計算受控外國企業所得適用辦法(個人CFC)」修正草案

- 【BVI公司】自2023年度起英屬維京群島公司需強制性提交年度財務報表

- 境外公司、香港公司與新加坡公司比較表

- 歐盟2024.02.20更新稅務不合作國家/地區名單將貝理斯與塞席爾移出黑名單

- 稅務機關可透過CRS掌握OBU之金流,以此作為CFC查稅依據

- 透過OBU進行理財投資,可選擇先排除FVPL評價損益至實現時課稅

- 【新加坡公司】新加坡所得稅法修正;新增10L條款針對出售海外資產收益徵稅

- 因應代理人Vistra/Tricor合併後的DD審查作業,維詮將著手推動現有境外公司轉換註冊代理人

- 中國大陸有可能因防制洗錢因素凍結透過走匯款公司管道之個人匯款;新加坡金管局指示匯款公司暫停透過非銀行和非銀行卡管道向中國匯款

- 境外公司的DD、KYC是做什麼?由我國的洗錢防制法來看